As US markets digest the impact of the peak in inflation, what comes next?

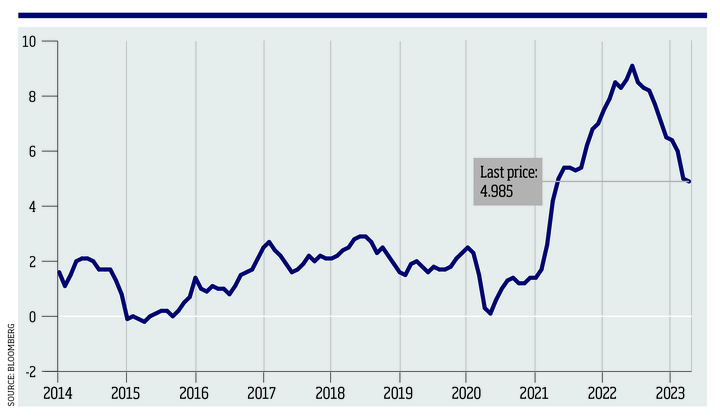

It is now very clear that the peak in US inflation is behind us, with CPI down from 9% in June 2022 to 5% in the latest - March - data point. The market's perception of inflation, meanwhile, has evolved from transient to entrenched and now peaking, which highlights the inability of forecasters to accurately predict economic data.

Bank of England's Bailey: QT not to blame for banking turmoil

Of the various potential scenarios, it is most likely that data will continue to moderate over coming months, but it is not clear yet how and when we will get back to the US Federal Reserve's 2% target.

In particular, core inflation is sticky and will take longer to come down than the headline number. When broken down, the shelter component, made up of rent and owners' equivalent rent, comprises a large portion of the overall figure.

Changes in rent happen slowly and the way the data is calculated makes it lag further. So, even as we see much lower numbers ahead, we are unlikely to see the Fed sustainably meet its 2% target any time soon.

US Consumer Price Index 2014-2023

Inflation is fundamentally important for the level of peak rates. With a much-improved inflation backdrop, it seems likely the Fed will hike by 0.25% in May and, furthermore, that this will likely be the peak for this cycle.

When we translate this backdrop into the equity market, we see that indices have generally been rising, with the likelihood of imminent peak rates and lower bond yields ahead.

It is important to mention that economic data has been much more resilient than feared with the US consumer, in particular, holding on as the labour market remains strong.

BoE governor Bailey signals further rate hikes in face of inflation uncertainty

This could seem like a perfect, even Goldilocks, backdrop. Inflation has clearly peaked, bond yields are lower (although this is in part a financial distress construct) and expectations for GDP growth are holding at moderate levels.

The reaction of the US market to chase growth stocks, technology and the Nasdaq Index in 2023 to date would seem to corroborate this notion.

Somehow, it is not quite this easy. Yes, inflation has peaked and rates will peak soon, but economic growth lags changes in monetary policy by several quarters and so the impact of 4.75% of rate hikes has still to be felt by the real economy.

The fact that US consumers continue to spend their higher-than-usual savings complicates the picture, but as savings fall over the course of the year it is likely that consumption drops.

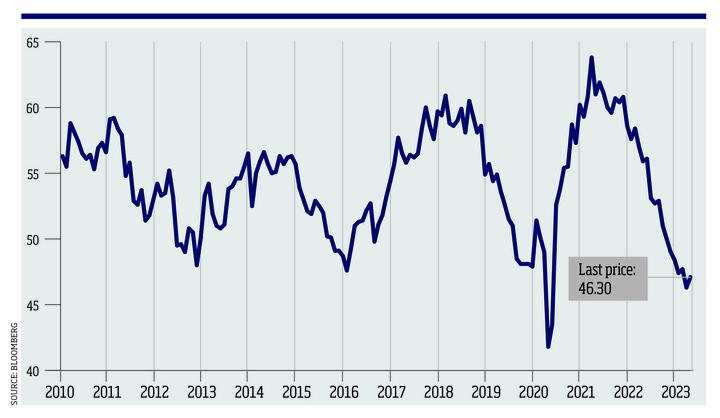

Elsewhere, there are also concerns; the ISM index is well below the 50 mark (indicating that the industrial arena is contracting) which in turn would finally start to soften the very robust labour market.

ISM index 2010-2023

Party mode may well continue for a while longer as we digest the peak in inflation, but the likelihood is that, as economic reality asserts, a period of volatility is ahead as macroeconomic data deteriorates beneath us.

The time-lag between peak rates, deteriorating data and the consequent inevitable easing is quite hard to predict but is highly likely to generate a whole range of opportunities as volatility gives new entry points in a variety of more cyclical sectors and stocks.

The variation of portfolio risk through the economic and monetary cycle is incredibly important and while we wait for these big questions on inflation, yields and GDP data to be answered, it is appropriate to run our portfolios in a more nuanced way.

This means there could be many opportunities to take advantage of that are likely to present themselves in the gulf between the last rate hike and the first cut.

Mike Willans is head of equities and Bimal Patel is senior fund manager, global equities at Canada Life Asset Management