The world was rocked last Thursday (24 February) as Russia began a full-scale invasion of Ukraine. The immediate reaction from markets was a sea of red across indices as the FTSE plummeted over 200 points that morning and Brent oil prices hit $105 a barrel.

"The Russian invasion of Ukraine will decimate global stockmarkets," was the response from Antonia Medlicott, finance editor at the financial comparison website, InvestingReviews.co.uk. However, Susannah Streeter, senior investment and markets analyst for Hargreaves Lansdown, offered a more measured view stating: "The shock of conflict is devastating, but history does point to relatively short-lived volatility on financial markets".

As markets went haywire members of the industry, while also grappling with the devastating development on a human level, scrambled to figure out the impact of the invasion on their investments and products.

In early trading following Putin's speech launching a "special military operation" to demilitarise and "de-Nazify" Ukraine, the MOEX index plummeted 45%.

Last week Western leaders had been attempting an economic war on Russia, opting for sanctions in order to weaken Russia's economic base and therefore limit the Kremlin's ability to finance war.

These sanctions will likely have a strong impact on market liquidity, on Russia and Russian related securities, according to Gregor Hirt, global CIO of multi-asset at AllianzGI.

"Substantial outflows from any related Russian instruments could ensue, and there could be knock-on effects for widely used instruments such as ETFs and derivatives," he explained.

Index and ETF providers are keeping a close eye on developments. If sanctions prevent foreign investors from holding Russian assets they will have to act swiftly.

At time of writing (24 February) Bloomberg Index Services had confirmed it would wind down three of bonds within its indicies due to US sanctions. The bonds would "exit the projected universe of our fixed income indices in March 2022 and will not contribute to the April 2022 returns universe," the group said.

MSCI said it was "closely monitoring Russia/Ukraine developments" and would analyse the "investability and replicability of the MSCI Russia Indexes" in light of new sanctions.

"Based on the outcome of this analysis, MSCI could potentially implement changes in the MSCI Equity Indexes, such as a security freeze for specific companies or a full deletion of specific companies from the MSCI Equity Indexes," the group said.

It added that it would also "closely monitor" the accessibility of the Russian equity market and "any material deterioration of accessibility" could lead to a "reclassification of the market subject to prior public consultations".

FTSE Russell said it was continuing to the monitor the situation and "will issue a further notification in due course". S&P Global said it could not make any comment on potential future index changes.

Movement by the index providers will have a knock-on impact on ETFs.

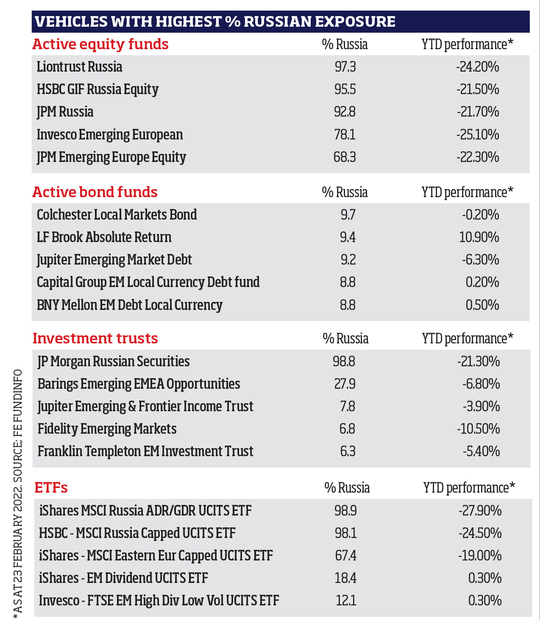

According to FE fundinfo, iShares holds three ETFs with the highest allocation to Russia, with a total $1.3bn of assets under management, according to the latest factsheets.

"BlackRock continues to communicate with and coordinate with industry and ecosystem stakeholders including index providers," the group said. "Actions that impact index designs will be assessed and BlackRock's actions will be taken with the goal of minimising impact to client holdings and to avoid, to the extent possible, any significant market disruptions."

Recent developments could also have a longer-term impact on Russia's categorisation in indices, according to Kunjal Gala, emerging markets portfolio manager at the international business of Federated Hermes.

"There is a big picture question - whether Russia is indeed an emerging market and the events over the last few weeks have certainly demonstrated that the economy is not moving in the right direction," he commented.

According to FE fundinfo 427 funds within the Investment Association universe have exposure to Russia, however only 23 have more than 10%.

However, not all investors with Russia exposure were concerned.

Chetan Sehgal and Andrew Ness, portfolio managers of Templeton Emerging Markets Investment Trust, which holds 6.3% in Russia, remained confident in the companies they held.

"We retain conviction in our holdings so long as sanctions and tensions do not a) bar us from owning or deriving benefit from such names, or b) significantly increase costs associated with the ownership of specific securities," they said.

The managers said that lessons from prior Russian military action were "insightful".

"In 2014 our emerging market strategies held a significant overweight in Russia, which coincided with the Russian invasion of Crimea in February that year," they said. However, while the index fell 20% following the news, within nine months the index reached a new high up 30% from the March lows, the pair explained.

Indirect exposure

While direct exposure to Russia is likely to be limited for some investors, they need to aware of their indirect exposure, flagged David Coombs, fund manager of Rathbone multi-asset portfolios.

Investors need to consider "the companies which might have underlying exposures - perhaps in the form of revenues or production facilities in Russia, to ensure you are comfortable with the level," he said.

Unsurprisingly, companies that have ties to Russia were already suffering at the end of last week. Shares in the FTSE 100 listed mining company Evraz, controlled by Russian billionaire Roman Abramovich plunged 30% on Thursday morning. Meanwhile, London listed Russian gold miner Polymetal was down more than 38%.

Investors were also reminded of BP's Russian ties. The company has a 19.8% shareholding in Rosneft, meaning the company fell following Putin's move despite surging oil prices. It has since announced it will offload the stake.

Oil, which was already at high levels thanks to "underlying bullish fundamentals" has the potential to hit $110 a barrel or even $120 as military conflict "exacerbates the existing imbalance between supply and demand," according to Victoria Scholar, head of investment at interactive investor.

However, Coombs warned that exposure to Russia is "not always about listing".

"Investors should be looking beyond the obvious and also thinking about second order impacts for example, if any energy supply disruption and/or price increases are more focused on Europe, how does this impact the European consumer and their disposable income?"