The build-up of Russian troops on Ukraine's borders has dominated the headlines over past weeks. With investors keeping watch for what happens next, we have looked at what may happen if the stand-off escalates into a hot war, says Damian Handzy, managing director - Analytics & Research at Investment Metrics.

The Nord Stream II pipeline, intended to carry 55 billion cubic meters of natural gas from Russia to Germany, is already in jeopardy. Energy prices will spike even higher. Russia may turn off the existing supply of natural gas to Europe in response to sanctions.

Western powers point to crippling sanctions including the removal of Russian access to the SWIFT financial network. This is the thing that will affect investors the most. It has the power to generate widespread impact on international trade and expectations for growth.

For now, markets are not signaling an imminent invasion - if they were, we'd expect a number of clear signals including a strong flight to quality (US bonds) that would raise prices and therefore lower yields. We'd also expect spiking energy prices, falling stocks (especially European) and strong movement in ruble currency options. While some of these markets have moved modestly, there is currently no consensus.

To simulate the reverberating impact that open war might have, we examined the fallout from the Russian default and subsequent ruble collapse in August 1998.

1998 and all that…

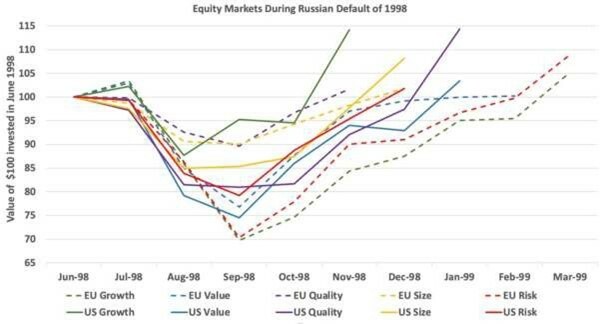

The first six months of 1998 had been good for investors. European stocks had risen 25% and the US stocks were up 48% (the dot com bubble was still more than a year away from bursting). When Russia defaulted on its debt and the ruble collapsed in August, both markets suffered similar losses of around 14% that month. US stocks bounced back within 3 months, fueled by roaring tech stocks, European stocks took six months to recover.

But there was a big difference in how individual factors performed.

US Growth fell sharply but bounced back fast and hard. European Growth fell twice as far and took more than twice as long to recover.

In contrast European Quality fell least and recovered quickly (within 3 months). US Quality did not, it fell nearly twice as much and took longer to recover.

Size made a difference. This was the factor for investors with a sensitive disposition. In both the US and Europe, the Size factor saw your portfolio fall modestly but recover to June '98 values by the end of November.

The laggards in terms of recovering value in the Russian crisis of '98 were Growth in Europe and Value in the US.

‘History doesn't repeat itself, but it often chimes'

While we shouldn't necessarily expect the same factor behaviour in 2022 if there is a Russian market meltdown, a reminder of how different European and American markets can behave is helpful.

Quantifying the long-term market and economic impact of a full-scale Russian invasion of Ukraine to the geopolitical world order is fraught with uncertainty. But it's safe to say that Europe would dramatically increase its military spending, prioritize energy independence from non-NATO countries and financial markets would take a hit with investors retreating to risk-off mode for the foreseeable future.

We would also not expect equities to bounce back as quickly as they did in 1998: a default by a country is one thing and open warfare is quite another.