Claire Trott (pictured) takes a look at the decline of QROPS transfers, assessing the pros and cons of the scheme...

Qualifying Recognised Overseas Pension Scheme (QROPS) transfers are something that HMRC have historically been very interested in, ensuring that they are not just being used to extract tax relieved funds from the UK, avoiding lifetime allowance charges. With the reduction and freezing of the lifetime allowance you might think this risk would increase, but this doesn't appear to be the case.

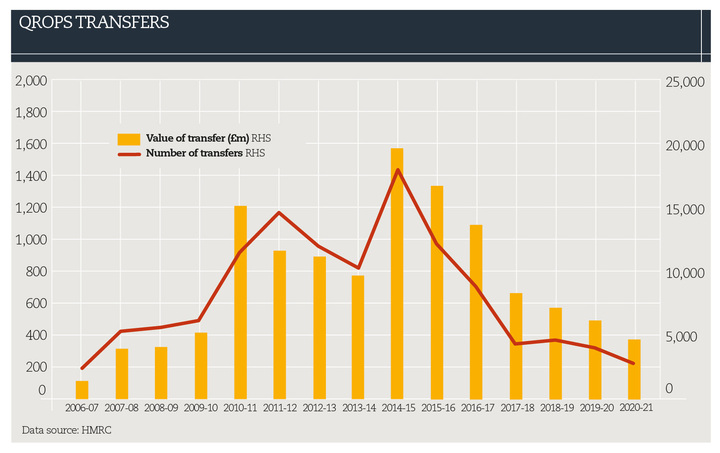

HMRC recently published the most recent information available about transfers to QROPS. In 2019/20 the number of transfers fell to only 3,000 with a total value of £416m. This is the lowest number of transfers we have seen since 2006/7. We have seen a marked drop in the number and total value of transfers to QROPS since the peak in 2014/15, which will have been for a number of reasons:

One of the main reasons for the decline is because of the overseas transfer charge. This is a flat rate of 25% on the whole transferring fund where the funds and the member are not either both in the European Economic Area (EEA) or both in the same jurisdiction for countries not in the EEA.

It isn't just applicable at the point of transfer either, it must be met for 5 years, or the charge is retrospectively applied. This can mean that if a client isn't sure that they will remain compliant then it makes more sense to retain the funds in the UK.

The other factor was the introduction of the pension freedoms, allowing more flexibility with regards to income and lump sums, as well as with death benefits. Often the move to a QROPS was a precursor to moving to something even more flexibly, which is now not required.

Transfers to QROPS shouldn't ever be undertaken lightly, even if the client plans to retire overseas; they often return to the UK later in life when care or medical needs increase. If the funds are overseas, then this can mean they are less accessible, and advice can be difficult to obtain.

We have also seen changes in legislation in countries that operate in the QROPS market, making it harder for clients to invest as they see fit, or use an adviser or investment vehicle within the QROPS that they choose. The UK has no control over these schemes or the regulatory regimes they operate under.

This also means that any protection that would have been afforded a client within the UK is lost, making them at greater risk of scams and excessive charges. Although less likely, it is also possible for the scheme to change its rules and failing to meet the rules for QROPS again puts clients at risk.

It is clear to see why the number of QROPS transfers are declining. It is a shame there isn't the same level of data with regards to the number of schemes returning to the UK, however the anecdotal evidence is that this is increasing, and I suspect it will continue to in the future as clients retire and want to simplify their investments.

There are clearly good reasons to transfer to a QROPS, especially for those returning to their home country following time working in the UK. Ideally it would be a standard scheme in the country in which they are returning to, but this isn't always possible and hence why the use of a specialist QROPS provider makes sense in these circumstances.

Claire Trott is divisional director - retirement and holistic planning at St James's Place